Samsung’s 2026 Labour Dispute: Supply Chain Lessons for Memory and SSD Buyers

- In March 2026, 93% of 66,019 Samsung workers voted to authorise strike action over wages and profit-sharing

- Workers were benchmarking against SK Hynix, where employees secured approximately $900,000 in annual bonuses

- A planned 18-day strike by ~48,000 workers — set to be the largest in Samsung’s 56-year history — was averted on May 20 via direct government mediation

- Full deal terms: 10.5% of semiconductor operating profit as stock bonuses + 1.5% in cash + 6.2% average wage increase, running for 10 years subject to profit targets

- The bonus disparity is stark: memory chip workers average ~$340,000–$400,000; non-chip employees receive approximately $4,000

- SECU minority union (~13,000 workers) has filed a court challenge; post-deal resentment is already causing work slowdowns in Samsung’s foundry and packaging divisions

- For buyers: tighter availability, shorter quote windows, and a new risk in Samsung’s foundry/HBM capacity are the practical near-term concerns

Samsung Electronics came within hours of the largest production disruption in its 56-year history in May 2026. What started as a wage negotiation in late 2025 escalated into a credible threat of an 18-day strike by nearly 48,000 workers at one of the world’s most important semiconductor manufacturers.

The strike was averted. But the situation has not fully closed: internal resentment over the bonus settlement is already affecting Samsung’s foundry and packaging divisions, with decision-making on major projects reportedly at a standstill. For infrastructure buyers who depend on Samsung DRAM, NAND, enterprise SSDs, or HBM, the story is still developing.

What Happened: The Timeline

| Date | Event |

|---|---|

| Late 2025 | Wage negotiations begin; collapse without agreement |

| March 18, 2026 | 93% of 66,019 workers vote to authorise strike action |

| April 23, 2026 | ~40,000 workers rally at Samsung’s Pyeongtaek chip complex |

| May 19, 2026 | Workers reject one-time bonus offer; demand annual recurring profit-sharing |

| May 19–20, 2026 | ~15 hours of talks; government threatens emergency arbitration |

| May 20, 2026 | Labour Minister Kim Young-hoon mediates; 10-year deal reached; strike suspended |

| May 27, 2026 | 74% of 62,616 workers approve the deal |

| May 29, 2026 | SECU minority union (~13,000 workers) files court challenge |

Workers in Samsung’s semiconductor division demanded a profit-linked bonus structure comparable to what SK Hynix had given its workforce — approximately $900,000 in annual bonuses per employee. Their specific ask: 15% of Samsung’s annual operating profit allocated as bonuses, plus removal of the 50% cap on annual salary bonuses and a 7% wage increase.

Samsung’s semiconductor division had generated record profits during the AI-driven memory boom — turning the company into a $1 trillion market cap business — but workers argued the bonus structure did not reflect their share of that value creation. An initial management offer of a one-time payment was rejected. Workers specifically demanded a recurring annual structure, not a lump sum.

| Component | Details |

|---|---|

| Profit-sharing bonus | 10.5% of semiconductor division operating profit — paid as stock |

| Cash component | Additional 1.5% of operating profit — paid in cash |

| Wage increase | 6.2% average salary increase |

| Duration | 10-year programme |

| Profit targets | ~$134B/year (2026–2028); ~$67B/year (2029–2035) |

74% of 62,616 participating workers approved the deal on May 27. Samsung is expected to distribute up to $26.6 billion in total bonuses to chip-division staff.

The deal created a sharp internal divide. Memory chip workers stand to receive an average of $340,000–$400,000 in bonuses. Workers in Samsung’s consumer electronics, smartphone, and TV divisions — represented by the minority union SECU — are in line for approximately $4,000.

That 100x disparity is why SECU filed a court challenge and why the situation is not as resolved as the headline approval suggests. Bloomberg reports that resentment has spread into Samsung’s foundry and chip packaging (TSP) divisions, with work slowdowns already under way and decision-making on major projects reportedly halted. This is the most current development — and it directly affects buyers who depend on Samsung foundry capacity or HBM delivery schedules.

What This Means for Memory and SSD Buyers

Memory and storage procurement already operates under sustained demand pressure. AI infrastructure buildouts, enterprise server refresh cycles, and cloud capacity growth are driving strong demand for server DRAM, NAND, HBM, and enterprise SSDs. The Samsung dispute adds a labour-side variable that most procurement strategies do not account for.

When a dominant manufacturer like Samsung faces credible production risk, buyers typically see four effects.

Availability becomes less predictable. Markets react to risk before production actually stops. Procurement teams accelerate orders, distributors tighten allocation, and quote validity windows shorten. This can happen quickly — often faster than a procurement process can respond.

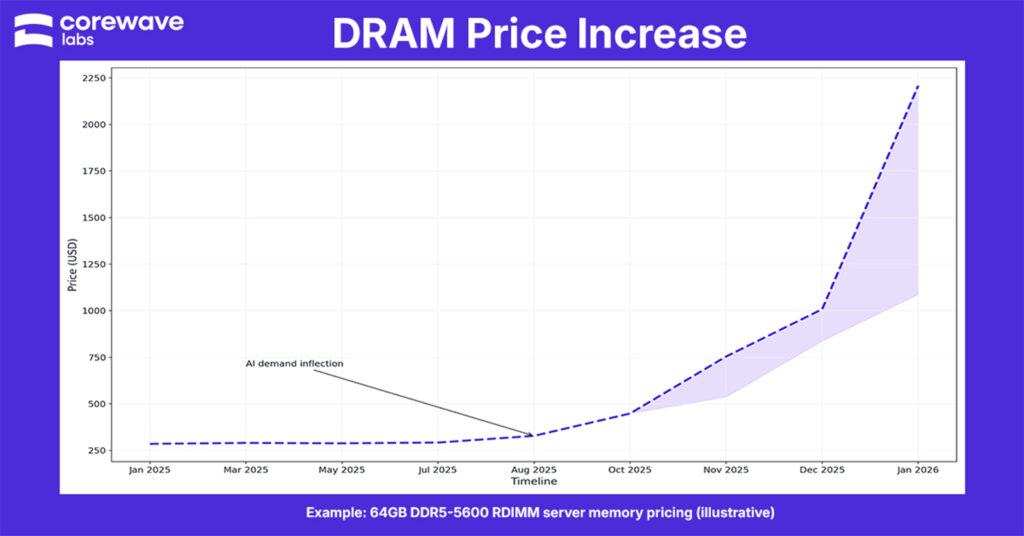

Pricing pressure increases. Supply-side risk at a dominant manufacturer shifts pricing power toward sellers. This is especially relevant for DDR4, DDR5 server memory, NVMe enterprise SSDs, and high-density storage configurations. See our DRAM price outlook for 2026 for current market context.

Lead times lengthen. Projects that depend on specific part numbers, OEM-compatible configurations, or validated memory modules are more exposed when supply chain predictability drops.

Single-vendor dependency becomes a liability. Infrastructure teams that have pre-approved only Samsung components for their server platforms lose flexibility exactly when flexibility matters most. Multi-vendor compatibility planning done in advance becomes a practical advantage.

Foundry and HBM risk is now a separate concern. The post-deal resentment affecting Samsung’s foundry and packaging divisions introduces a new layer of risk for buyers of HBM and custom chip products that were not directly part of the original labour dispute.

Five Supply Chain Lessons

Market Outlook

Frequently Asked Questions

Conclusion

The Samsung 2026 labour dispute is a case study in how supply chain risk has evolved. The threat was not a natural disaster, a geopolitical event, or a manufacturing failure. It was a disagreement about how profits are distributed when a commodity becomes strategic infrastructure — and the fallout from the resolution is now creating a different kind of risk in Samsung’s foundry operations.

For infrastructure buyers, the response is disciplined procurement planning: validate alternatives before you need them, maintain multi-vendor compatibility lists, monitor lead times, and work with partners who can source reliably across manufacturers. Preparation is not a reaction to a crisis. It is how you avoid one.

CoreWave Labs supplies enterprise server memory, SSDs, HDDs, and networking hardware to data centres, telecom operators, cloud providers, system integrators, and trading companies worldwide. We source verified components from Samsung, Micron, SK Hynix, Solidigm, Western Digital, Seagate, and other enterprise-grade manufacturers.

Need to verify compatibility or secure supply for an upcoming project? Request a quote or view current pricing on our Memory Pricelist and SSD Pricelist.

Further Reading

Samsung DDR5 RDIMM Part Number Decoder

How a Strait of Hormuz Disruption Could Impact the Semiconductor Supply Chain